the MoneySmartLife.org Lifestyle blogEmpowering sustainable financial well-being for working class families

|

|

Holidays are times of gathering for families. As such it provides opportunities to help the extended family strengthen its economic foundation. These are the perfect times to discuss estate plans, elder care, custodial expectations and more. Now that sounds pretty heavy and it may be depending upon how your family views these subjects. But not talking about it isn’t wise.

Normally estate matters are resolved as part of a process that takes time to complete. But they must be started. Start with the easy stuff. Are wills in place for all adults 18 years and older? What happens to the kids? Are there durable power of attorneys and health care directives in place for all adults 18 years and older? It is better to have these discussions before a crisis requires them. Not having proper estate plans in place has put significant stress on family relationships regardless of assets forever. Yours will be no different. Take the next steps depending on what is learned. Help those that have no plan get one written and recorded. Encourage those that have a partial plan to upgrade. Lead by example. Family gatherings can also provide opportunities to save money through the elimination of redundant streaming services expenses. Most streaming services allow for multiple profiles or device logins. Maximizing profiles used for each service and spreading the cost of the subscriptions can expand extended family access while lowering individual unit costs. This is also a time to review subscription services already shared to see if they are still used and eliminate those that aren’t. Some services can be eliminated seasonally depending upon demand. The family can adopt a “binge and go” strategy. This is where a service is subscribed to for a period of time to allow episodes to be binged. The effect is to make the service disposable, use it then lose it. This eliminates autopilot spending that subscriptions require. Here is a list of some popular subscription streaming services and links to their multiple user policies:

0 Comments

Power outages and interruptions happen. If they happen often enough or for long enough you could be eligible for compensation from DTE and Consumers Energy. The Michigan Public Service Commission (MPSC) Service Quality and Reliability Standards requires utility companies to compensate customers for losses associated with power outages. Rules regarding outage service credits and eligibility requirements can be found in the MPSC’s Service Quality and Reliability Standards. These standards provide customers a $25 credit upon request if the utility’s investigation of your request determines you have experienced a qualifying outage.

There are 3 types of available credits:

An investigation will be conducted and a decision will be rendered within 30 days. Your claim will be summarily denied if:

Financial shocks are inevitable during a lifetime. “Stuff happens,” according to the PG-rated version of that cliche. When it does, my language is more NC-17. Nevertheless, happen it does. The most common financial shocks for working-class families are:

What is an emergency fund? It is a “liquidity buffer” between you and ruin. If you have very little saved — say $200 to $500 — each additional dollar you set aside dramatically reduces your likelihood of falling into financial hardship. It can be any of these items. Some are decidedly better options than others:

Forget the 3 to 6 months of take-home pay that is commonly parroted throughout financial media and literature. This goal is often unattainable for low-income wage earners. A more realistic minimum target is $2,467. A fund of this amount will be sufficient for most emergencies. Having such a fund stops you from getting stuck with short term remedies with long term consequences like being late on rent or borrowing from a payday lender. Often creating a cycle of cash draining late fees and prolonged financial insecurity. Building an emergency fund is your #1 priority. You should well establish an emergency fund before you divert resources to the very prudent debt reduction strategy necessary for your long term success. You should continue or start making all minimum payments on time and continue to do so until your emergency is well funded. Debt reduction is achieved by consistent application of payment to the principal balance. Having an emergency fund will let you maintain a good payment history so you won’t have to “rob Peter to pay Paul” when the inevitable happens. One missed credit card minimum payment can close off what may be a critical asset during a financial emergency and put a big hole in your safety net. Modified universal default terms may render a late payment to one lender a catastrophe in your creditworthiness regardless of your actual payment history. Your ability to borrow should be viewed as part of your safety net. It creates capacity and demonstrates financial capability. Your credit card cash advances and spending limits are critical components that can help mitigate some of the impacts of an emergency while buying you time. An excellent credit score can give you immediate access to additional money during an emergency. It is a MoneySmartLife strategy to responsibly and proactively expand your borrowing capacity annually. Just as your net worth expands annually, so should your credit capacity. They weave your safety net tighter and softer.

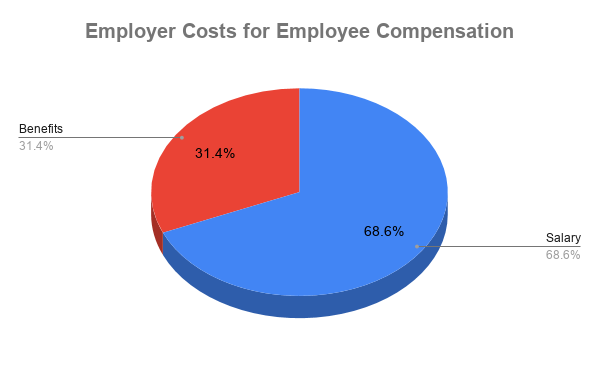

Most employees unnecessarily leave money on the table when it comes to their compensation by not maximizing their employer-provided benefits. According to the BLS, 30% of your compensation is benefits. Let’s look at some strategies to get the most out of your benefits for the rest of this year.

But first a rant about paid vacation days. I realize that 1 in 4 American workers don’t get any paid time off at all. The rest get paid vacation “yet only 51% of paid vacation days are used! More disturbingly (if not surprisingly), 61% of those who do take vacation are “working while on vacation.” Americans left 768 million days of paid time off unused last year, according to research released by the U.S. Travel Association. The study found that 55 percent of Americans did not use all of their paid vacation time.” Why would you do that? Seriously, ask yourself, “why would I do that?” What are the short/long term benefits of this behavior? Here is what to do for the rest of this year. The best time to do this is around October 1. This will give you flexibility before that end of the year time crush everyone experiences. Also, it gives time for any changes in your withholding strategies to take effect and return the expected benefits. Of course, these strategies can be implemented anytime.

|

Archives

May 2020

Categories

All

|

RSS Feed

RSS Feed